Ondas Inc ($ONDS) Q4 2025 Earnings Breakdown

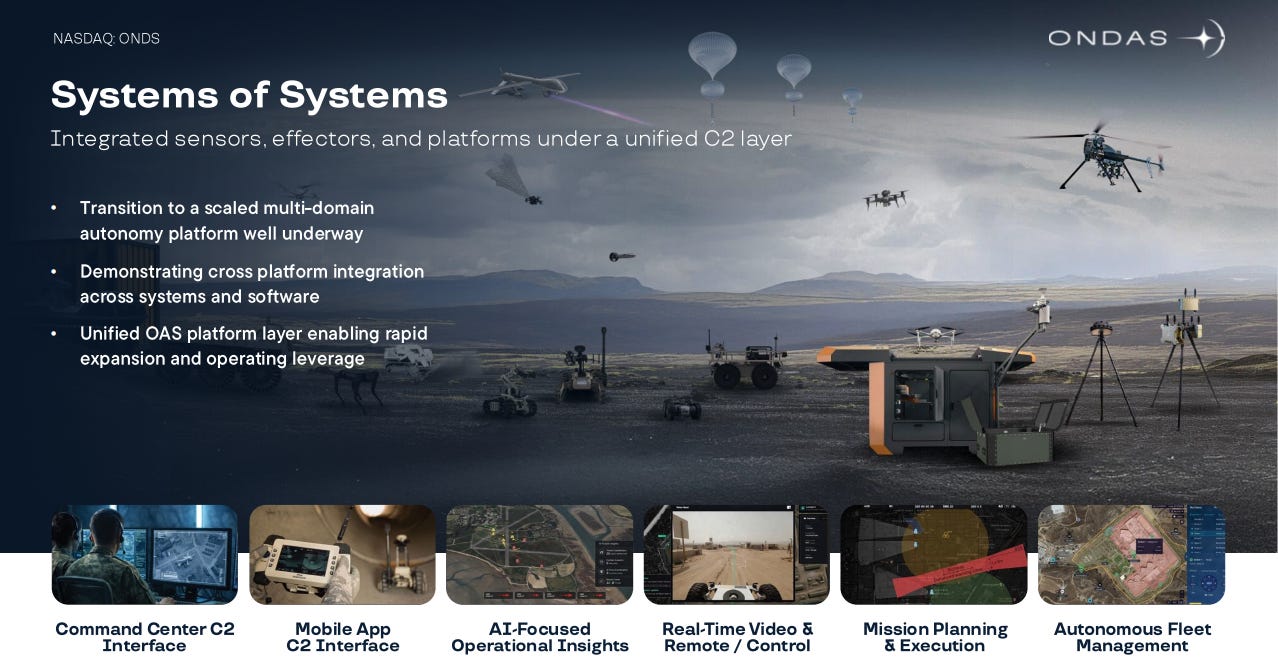

An Emerging System of Systems Leader In Drones

The Ondas’ Story Is Still In It’s Prologue

On paper, ONDS 0.00%↑ completely blew earnings out of the water, with over 600% YoY growth and massive new revenue targets. What also stood out was the fact that Ondas is growing into a system of systems solution provider of an entire autonomous stack for air and ground solutions at the perfect time when drones are at the top of every headline. Revenue is ramping, backlog is growing, margins are improving, and management is clearly trying to use its balance sheet to build a much larger multi-domain business before the broader market fully appreciates what is happening. All of this in the last 3 months. The kicker? The stock is currently cheaper than it was to start the year making it one of my primary acquisition targets.

Financials

Ondas reported Q4 revenue of $30.1 million, up sharply year over year, while full-year 2025 revenue came in at $50.7 million. More importantly, the company raised its 2026 revenue target to at least $375 million and established a Q1 2026 revenue target of $38 to $40 million. Management said their cash position stood at roughly $1.5 billion, with shareholder equity climbing to about $441 million from roughly $17 million the year before. The company also emphasized that the January 2026 financing was led by a large institutional investor and that it is pursuing broader index inclusion, including the Russell 2000. While they are flush with cash, they are not using it for aquisitions. The Ondas acquisition strategy has mainly revolved around share offerings which is scary for many investors due to dilution risk. While I agree that dilution is never what you want to see, the fact that they are keeping their balance sheet this healthy means they have a lot more flexibility than any other company at their market cap in the sector giving them options. This is going to allow them to survive in many uncomfortable market spaces and edge out competitors. It is a good thing long-term.

Key Acquisitions

One of the big takeaways was CEO, Eric Brock, laying out an aggressive acquisition-driven growth plan, which was a huge reason why the 2026 target jumped so dramatically. Across the recently announced deals, Ondas said it expects roughly $230 million of 2026 revenue contribution (from acquisitions), with key additions including Mistral, BIRD, Rotron, INDO Earth Moving, and World View. The company also highlighted that these acquisitions bring in revenue, but also manufacturing capability, customer relationships, geographic access, new end markets, and, in some cases, prime contractor exposure (Mistral).

BIRD looks especially important near term because it brings mission-proven airborne missile protection and ISR technology already deployed across more than 700 aircraft and 40+ aircraft types. This gives Ondas exposure to a higher-value protection layer and more durable defense program budgets, which should help both revenue quality and margin profile over time.

Mistral, my favorite aquisition to date, is central to the U.S. expansion thesis. Management described it as a direct accelerant for the Ondas’ U.S. market push because it adds manufacturing and program execution capability while also expanding access to larger defense programs due to their clearance. Mistral has seen long-term success in Pentagon lobbying, shown recently with their $1 billion dollar Uvision contract they helped broker for loitering munitions. This relationship is key for Ondas’ success domestically.

Rotron was another big one and expands the strike and propulsion side of the platform, particularly as NATO and allied governments increasingly prioritize low-cost, autonomous systems. Rotron adds another layer of system stacking with drones capable of carrying other drones by air, reducing the need for human piloted air/ground transport thats risky and expensive. They also provide a window into long-range loitering munition solutions, something Ondas was lacking before their Mistral acquisition.

INDO Earth Moving was another acquisition, more niche in my eyes. It gives Ondas an entry point into military engineering vehicles and another layer of ground capability. My thought is they will use this business in tandem with their demining capabilities through 4M defense and their partnership with SPAI 0.00%↑. Demining is largely untapped as a market and is valued at over $10 Billion dollars. One of the many revenue sources Ondas is targeting.

The key takeaway is every acquisition since 2025 has had meaning and accomplished something where the business was lacking. As an investor, this is key. I need to know that management is working in the shareholders best interest long-term. These acquisitions all help to secure the final vision of what ONDS 0.00%↑ plans to be - a defense prime and municipal infrastructure giant.

New Partnerships

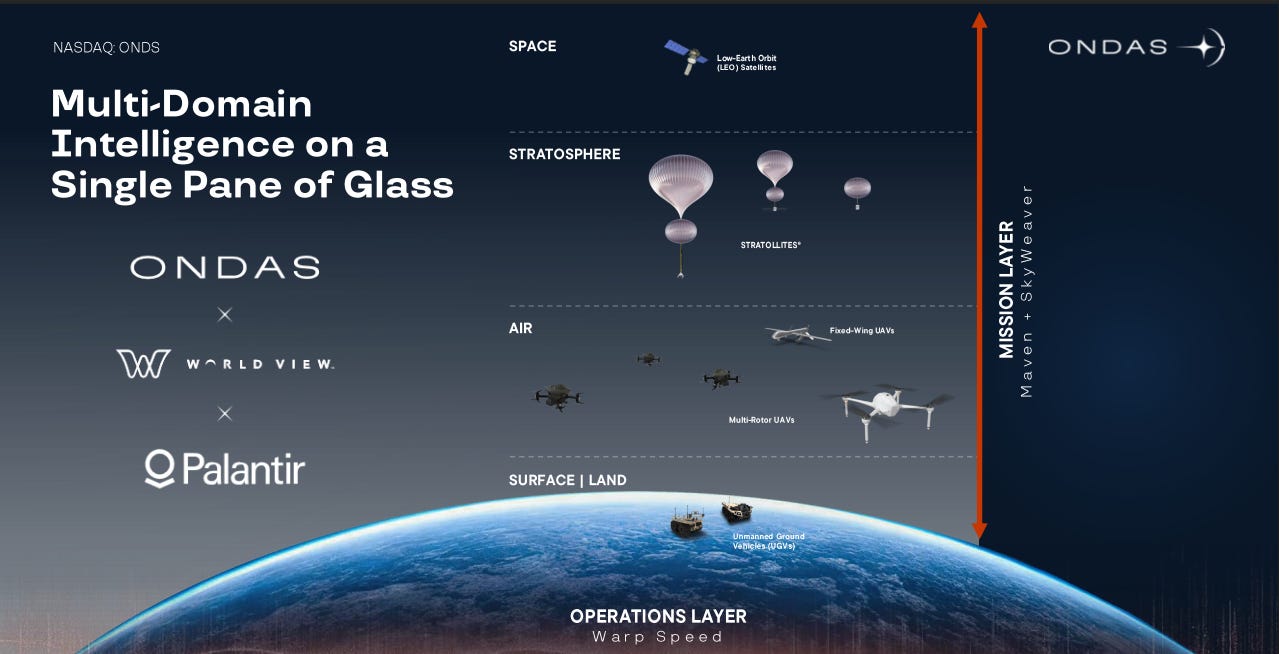

World View and Palantir

If there is one section of the Ondas story that has the potential to capture the market’s imagination, it is probably the combination of World View + Palantir + Ondas. Ondas’ March partnership with World View was already interesting because it added the stratospheric sensing layer to the company’s broader ISR vision. The follow-up partnership with Palantir made the strategic direction much clearer. The companies said they are working to build AI-enabled, multi-domain ISR capabilities that connect stratospheric, aerial, and land-based systems into a more unified command-and-control and intelligence framework. World View’s Stratollite platform is designed to operate in the stratosphere for long-duration sensing missions, filling the gap between satellites and conventional aircraft. Palantir’s AIP, Warp Speed, and related operational tools are meant to help scale production, mission planning, and edge intelligence for those missions. Ondas’ role is to connect that stratospheric layer with its growing autonomous aerial, ground, and counter-drone portfolio. This is still early, and investors should treat it that way. But if this ecosystem begins converting into real programs, it could become one of the most differentiated parts of the Ondas narrative. It moves the company closer to being viewed as an integrated autonomy and ISR platform with potential entries into Golden Dome contracts rather than just a drone and C-UAS focused stock.

ONBERG

Another underappreciated piece of this story is the ONBERG joint venture with Heidelberg. Ondas and Heidelberg said ONBERG is intended to become a European one-stop shop for autonomous drone defense systems, with an initial focus on Germany and Ukraine. European defense buyers increasingly want sovereign-aligned production, local support, and regional industrial capacity. Ondas is trying to position ONBERG as the answer to that requirement. This matters because Europe is entering a growth cycle - spending more on defense; it is also becoming more focused on who builds, services, and supports those systems locally due to current geo-political upheaval surrounding NATO. If ONBERG scales the way management hopes, it could give Ondas a meaningful foothold in one of the most important defense growth markets outside the United States. Eric also noted that ONBERG’s potential upside is not yet included in current revenue guidance, which leaves room for future surprises if execution is strong and we already know Germany likes their tech, with C-UAS orders already active accross airports in the region.

The Pathway to Profitability

Ondas is not a profitability story today - you are buying into the idea of what could be. The company posted a large net loss, though management emphasized that $82.2 million of the quarterly impact came from a non-cash warrant revaluation tied to prior financing relieving worries. That accounting charge does not reflect the underlying operations of the business, but it will likely continue to create noise in reported GAAP earnings. What matters more is the timeline leadership laid out for EBITDA progression. Ondas said it expects its product companies to become EBITDA positive in Q3 2026, OAS in Q3 2027, and Ondas overall in Q1 2028, with the key possibility that these milestones could be pulled forward as scale improves. That timeline will ultimately depend on execution, integration, and whether the company can continue to convert backlog and demand into high-quality revenue. But it at least gives investors a framework for how management sees the operating leverage building from here.

Conclusion

Overall, ONDS 0.00%↑ posted a very strong quarter, over tripling their initial revenue target for 2026 and acquiring some truly transformational companies. The balance sheet is now large enough to matter and is one of the biggest tailwinds. The combination of BIRD, Mistral, ONBERG, World View, and Palantir gives Ondas one of the more ambitious multi-domain autonomy narratives in the small-cap market right now and I believe it is grossly undervalued. Regardless of what I believe, the market will still want proof. It will want to see the Q1 revenue show up, the acquisitions integrate smoothly, and the backlog continue to climb. But after this report, it is getting harder to argue that Ondas is just another speculative drone name. Leadership is building a system of systems for drones akin to nothing we have seen at this scale, and 2026 may be the year that story starts showing up in a much bigger way.

Disclosure

The information provided in this publication is for educational and informational purposes only. Nothing in this content should be interpreted as a recommendation, solicitation, or offer to buy or sell any security. I do not provide personalized investment advice or individualized recommendations. All examples, tickers, scenarios, and analyses are strictly for general educational discussion.

The views expressed are my own and do not represent the views, policies, or recommendations of any employer, broker-dealer, or affiliate. Any securities referenced are used solely as case studies to demonstrate research methods and analysis frameworks.

Investing involves risk, including the potential loss of principal. You are solely responsible for your own investment decisions. Consult a licensed financial professional for personalized guidance.