The Key Component Supplier Powering The U.S. Drone Gold Rush

By Hidden Gems Research LLC

As of 2026 the U.S drone market is entering its most important transition period of all time. Federal regulations are loosening in support of an aggressive legislation swing to keep up with the advancements in drone technology currently present in China and Ukraine. Remember Isaac Newton’s third law of motion: for every action their is an equal and opposite reaction. For every drone made there will need to be a drone or other technology to counter it, exponentially increasing the demand for NDAA compliant components which cannot be sourced from the largest (by far) component manufacturer - China. There is only one domestic small cap that foresaw this and has positioned itself to become a primary winner over the next 5 years. The cherry on top? Its currently trading at a 20% discount from recent highs a month ago on the cusp of massive drone DoW orders worth tens of millions. Let’s get into the company and key details you need to know before missing the ride up.

Unusual Machines UMAC 0.00%↑

Unusual Machines designs and manufactures drone components while operating a growing domestic production footprint through it’s main drone component catalogue and two key brands. The first being Fat Shark - a legacy leader in FPV video systems, headsets, and drone electronics. These are all key control mechanisms for FPV drones currently becoming increasingly popular for reconnaissance and scouting initiatives for first responders and military combatants. They will likely be a necessity for any boots on the ground squads in the future due to their importance in attaining intelligence and mitigating unseen threats before they become a problem. The second is Rotor Riot - an e-commerce distribution platform and community hub for drone pilots and builders. This sales channel specifically has grown 30% YoY for the last several years, greatly increasing Unusual Machines’ exposure to industry clients and enthusiasts

$UMAC sells into individual consumer, hobbyist, enterprise, defense, and public safety channels. Recently its become clear that their main focus is shifting to the enterprise and defense side. This is due to them becoming a foundational supplier of NDAA-compliant drone motors, flight controllers, and FPV camera and video transmission systems - approved component stacks used in Blue UAS-aligned platforms which are the gold standard for government solicited orders. In a world where drone supply chains are being re-shored and foreign components are increasingly restricted, Unusual Machines is positioning itself as the domestic component layer that American drone manufacturers cannot scale without due to the lack of existing infrastructure. Exciting stuff, now lets talk numbers.

The Numbers: Revenue Growth, Orders, and Enterprise Acceleration

Unusual Machines is on the cusp of releasing Q4 2025 results so in the meantime we will look at Q3, which saw $2.13 million (+39%) YoY growth and the the last 3 cumulative quarters coming in at $6.3 Million (+55% )YoY growth. While not staggering, this has historically been a pre-profit company that has shown consistent momentum. Allan Evans, the CEO, noted in interviews that UMAC nearly doubled enterprise sales and drove margin improvement as enterprise orders became a larger share of the business. They also posted their first profitable quarter ever with improving gross margins driven by higher value previously mentioned enterprise demand. This doesn’t take into account DJI and other Chinese drone manufacturers being added to the FCC covered list in December 2025. This will restrict both foreign drones and components from being imported for NDAA compliant orders - massive for future revenue growth.

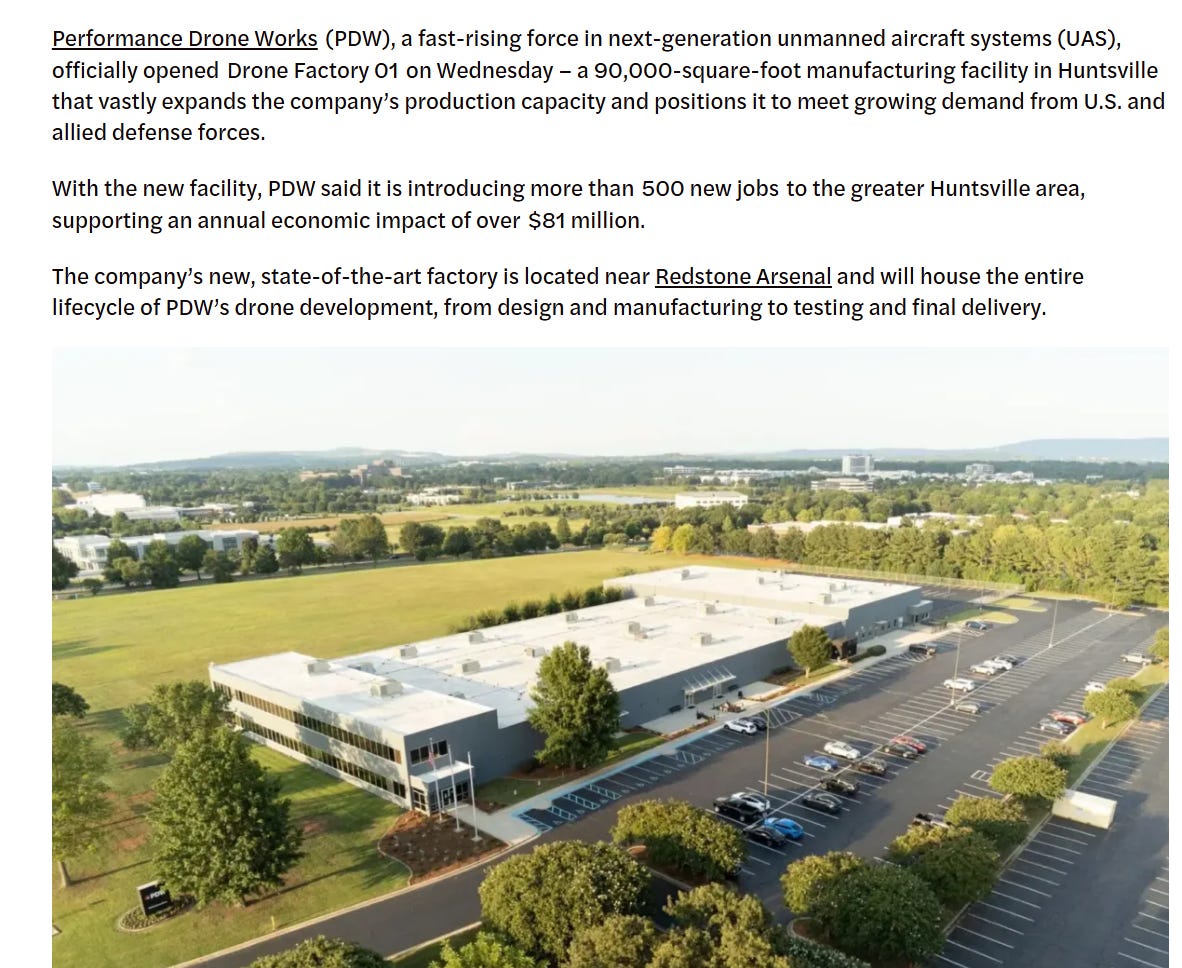

One of the most interesting orders was for $3.75 million dollars from Performance Drone Works, a fast-rising company with ties to the military and another popular company I love to cover: Ondas Inc ONDS 0.00%↑. The deal was for an initial order to kick off their relationship as partners where UMAC 0.00%↑ will be a strategic supplier for future scalable drone programs. This comes at the onset of PDW’s announcement of a new 90,000 sqft. drone manufacturing facility in Hunstville, Alabama - producing tens of thousands of drones per year. That’s a lot of components!

Upcoming Catalysts and Tailwinds: Unleashing American Drone Dominance

Aside from the FAA, the Department of War (DoD) has been one of the biggest advocates of domestic drone industrialization due to risks of being behind in the global race compared to other superpowers like China. To combat this they created the Drone Dominance Gauntlet - essentially a competition between small, non defense primes to see who can create the best product with the capability to scale it. This initiative will take place over a few months starting in February with contractors being eliminated in batches until a few winners remain who will receive long-term support and contract opportunities. Like the California gold rush of 1848, the biggest winners weren’t the miners themselves but the entrepreneurs who supplied the picks and shovels. In this case that is UMAC 0.00%↑. They have the capacity and opportunity to supply whoever the winners of this are. PDW, ONDS 0.00%↑, and RCAT 0.00%↑ all have partnerships with Unusual Machines, meaning if any of them win, UMAC is sure to benefit. They are also likely working on deals with other entities involved and have previous business with the Army itself. This gives them less risk and more opportunity then the companies providing end systems and potential bids with no guarantees.

These drones will require millions of components over the course if the next 2 years including motors, controllers, FPV headsets, powertrains, and replacement parts. Unusual Machines happens to be the largest domestic manufacturer for several critical component categories. No other company is positioned to capitalize off this opportunity in the same way, its a perfect storm and the timing is impeccable for this supplier

What are the Risks?

No bullish thesis is without it’s risks, especially in the world of small caps and emerging markets. With UMAC 0.00%↑ the main risk is scaling. The demand for these large quantities of drones is immediate and the offshore component suppliers of years passed have been pushed out. Unusual Machines is a relatively new company that isn’t scaled to its full potential. Allan Evans has been combatting this through massive procurement of new hires, infrastructure, and facility acquisitions but, due to the size of impending backlog, we wont know if its too little or too late until the full scope of demand is made clear. The good news is UMAC has made it obvious through previous interviews that they’ve scaled inventory ahead of demand. This is a liquidity risk in itself if no orders were received but a smart hedge if the thesis plays out how I think it will.

Conclusion

Unusual Machines is an industrial supply chain company being pulled into relevance by policy and procurement. The U.S. is re-shoring drone components the way it re-shored chips and is creating a regulated, NDAA pipeline that few have the facilities to capitalize on. UMAC 0.00%↑ is one of the only pure-play domestic suppliers already scaling production today. Ask yourself this - do you believe drones are becoming a national security priority and a domestic supply chain mandate? If yes, then the highest-leverage place to be is not necessarily the drone end system platform but part supplier inside every platform instead. Unusual Machines is building the domestic component backbone, we are still early, and the Drone Dominance wave is just beginning.

Disclosure

The information provided in this publication is for educational and informational purposes only. Nothing in this content should be interpreted as a recommendation, solicitation, or offer to buy or sell any security. I do not provide personalized investment advice or individualized recommendations. All examples, tickers, scenarios, and analyses are strictly for general educational discussion.

The views expressed are my own and do not represent the views, policies, or recommendations of any employer, broker-dealer, or affiliate. Any securities referenced are used solely as case studies to demonstrate research methods and analysis frameworks.

Investing involves risk, including the potential loss of principal. You are solely responsible for your own investment decisions. Consult a licensed financial professional for personalized guidance.